We adhere to strict standards of editorial integrity to help you make decisions with confidence. Some or all links contained within this article are paid links.

During your working years, it’s important to have cash savings for unplanned expenses. These could run the gamut from home repairs to medical emergencies to a period of unemployment.

But what if you’re retired and are therefore relying on your savings and investments to fund your lifestyle? In that case, the guidelines for keeping cash on hand change quite a bit.

Here’s what you need to know before you retire.

Why do retirees need cash?

In the context of retirement, cash can mean funds in a checking or savings account, or certificates of deposit (CDs) —essentially, money that’s shielded from market fluctuations.

Here are some reasons you’ll need cash as a retiree.

1. You’re living off of savings now

While Social Security offers income, the average benefit of $1,918 per month may not cover all expenses. Once that’s spent, cash allows you to handle surprises like car repairs or home maintenance without selling stocks or draining your savings.

If you want to grow your savings more efficiently, you can so just that with a high-yield cash account like the one offered by Wealthfront.

Wealthfront is a financial services platform offering a range of products, from automated investing to cash accounts. The Wealthfront Cash Account offers 5.00% APY — that’s 10x the national average.

With full access to your money at all times, Wealthfront also offers fast (and free) transfers to internal Wealthfront investing accounts, as well as external accounts

To compare all the best savings options, you can check out Moneywise’s Best High Yield Savings Accounts of 2024 to find some savvy savings options that earn you more than the national average of 0.4% APY.

Like the sound of high-yield account rates?

Then you might also be interested in exploring certificates of deposit (CDs). A CD is a low-risk savings option that can yield interest comparable to, or even higher than, the top savings accounts. The trade-off for this higher rate is that your money stays locked in the account for a set period.

For example, Discover offers CDs with competitive rates and terms ranging from three months to 10 years.

Currently, Discover’s 12-month CD offers a competitive 4.10% APY — significantly above the rate offered many large U.S. banks provide on similar accounts. Plus, Discover CDs have no fees, and there’s no minimum deposit required to get started.

2. You will face unplanned expenses

For workers, an emergency fund doesn’t just safeguard against a job loss. It can also be the ticket to covering surprise expenses without going into debt. And being retired doesn’t make you immune from surprises.

If you’re concerned that Medicare might not cover your expenses, there are other insurance options you can consider.

If you’re looking for a policy that will last a lifetime, with a locked-in premium and a cash value that can be tapped into while the policyholder is still alive, a whole life insurance policy from Mutual of Omaha is the right fit for you.

With coverage amounts ranging from $2,000 to $25,000 (in WA, $5,000 to $25,000), you can rest assured that you and your family will always be ready to cover those unexpected expenses.

It only takes five minutes to fill out an online application with your personal and beneficiary information. Once you register, not only will you be guaranteed coverage, but your benefits will never be reduced due to age or health. Plus, no medical exams or health questionnaires are needed to join.

If your health is excellent, you may be able to cover your health care expenses with relative ease. If you have multiple health issues, it’s a good idea to stockpile extra cash in case your bills start to mount at a time when it’s not advantageous to tap your investments.

3. You want to protect yourself from investment losses

You may have the majority of your retirement savings in a portfolio of investments that include stocks, bonds, and mutual funds. The upside of holding these investments in retirement is that they can continue to generate growth, giving you access to more money. The downside is that their value can change based on market conditions.

If you have a riskier portfolio more concentrated in stocks, then you may want more cash on hand to balance that out. If your portfolio is largely bonds, you might get away with less cash, since bonds are less volatile than stocks and can provide predictable interest payments that you can use as income.

If you’re optimizing your investments for stability, gold is typically more stable than stocks during economic downturns and recessions. In fact, gold has increased in value sevenfold over the last 100 years.

These things are especially important for retirement planning. For instance, by opening a gold IRA with the help of American Hartford Gold, you can invest directly in physical precious metals rather than stocks and bonds.

You’ll get expert guidance to help you navigate the complexities of setting up and managing your IRA, secure storage with IRS-approved depositories, and flexible investment plans tailored to your goals — plus, transparent pricing with no hidden fees.

Just as there are different opinions when it comes to building an emergency fund for your working years, the guidance varies over how much cash you might need in retirement.

Based on your expenses, needs, and investment portfolio, services like WiserAdvisor may help you find a financial professional who can strike the ideal balance in your portfolio so you have enough cash on hand without going overboard.

WiserAdvisor is a free service that helps you find a financial advisor who can co-create your financial goals. All it takes is a few minutes to answer some questions about yourself, and WiserAdvisor will provide you with a personalized match of two to three advisors from their database of thousands.

We adhere to strict standards of editorial integrity to help you make decisions with confidence. Some or all links contained within this article are paid links.

The Social Security system in the United States is in deep trouble.

According to the 2024 Trustees report, the Old-Age and Survivors Insurance (OASI) trust fund, which pays benefits to retirees and survivors, could be depleted by 2033, leaving it able to cover only 79% of obligations.

With time running out, experts and lawmakers are divided on solutions, from benefit cuts and raising the retirement age to expanding revenue sources. And U.S. President-elect [Donald Trump campaigned on a promise to cut income taxes]https://moneywise.com/retirement/trump-social-security-taxes-seniors), a move that could drain the program’s funds even faster than forecasted.

Labor economist Teresa Ghilarducci, a renowned thought-leader on U.S. retirement issues, believes there are “many easy fixes” — here’s what she recommends.

Expanding Social Security’s revenue sources

Ghilarducci believes the solution to Social Security’s challenges is simple: bring in more revenue.

“We are past the point where we can fix Social Security by cutting benefits,” she told Bloomberg. “That is a non-starter because the benefits for Social Security are keeping almost all of the people on Social Security… above the poverty level.”

But sitting above the poverty level isn’t exactly the stuff of hallmark cards. If you’re concerned that Social Security might not replace your income and fully support the retirement you want, finding a professional advisor through WiserAdvisor could help you create a stronger bankroll for your golden years.

WiserAdvisor is a free matching service that connects you with a pre-screened financial professional whose expertise is tailored to your goals. Just answer a few questions, and WiserAdvisor will provide a personalized recommendation of two to three advisors.

Building a solid nest egg is crucial for a secure retirement — especially if you want to rely less on Social Security.

Finance experts like Suze Orman have long touted the idea that by focusing on growing your retirement accounts and diversifying your investments, you can create a stronger financial foundation.

Equally important is having an emergency fund, which can protect your savings from unexpected expenses without jeopardizing your retirement goals.

Contribute to and diversify retirement accounts

In an era of economic uncertainty, securing your financial future may require a more proactive approach than in the past — one that goes further than old age security.

For instance, if you’re optimizing your investments for stability, gold is typically more stable than stocks during economic downturns and recessions. In fact, gold has increased in value sevenfold over the last 100 years.

These things are especially important for retirement planning. For instance, by opening a gold IRA with the help of American Hartford Gold, you can invest directly in physical precious metals rather than stocks and bonds.

You’ll get expert guidance to help you navigate the complexities of setting up and managing your IRA, secure storage with IRS-approved depositories, and flexible investment plans tailored to your goals — plus, transparent pricing with no hidden fees.

Make sure you have an emergency fund now and in retirement

While building personal wealth through smart, independent investing has never been more essential, it’s also important not to forget about putting aside an emergency fund — distinct from retirement savings so you don’t have to dip into long-term investments when unexpected expenses arise.

Daunting as it may be to think about, there are ways to manage your investments and your emergency fund in the same place that are less stressful and more hands-off than you would think.

You can check out Moneywise’s Best High Yield Savings Accounts of 2024 to find some savvy savings options that earn you more than the national average of 0.4% APY.

Like the sound of high yield interest rates? Then you might also be interested in exploring certificates of deposit (CDs).

A CD is a low-risk savings option that can yield interest comparable to, or even higher than, the top savings accounts. The trade-off for this higher rate is that your money stays locked in the account for a set period. For example, Discover offers CDs with competitive rates and terms ranging from three months to 10 years.

Currently, Discover’s 12-month CD offers a competitive 4.10% APY — significantly above the rate offered many large U.S. banks provide on similar accounts. Plus, Discover CDs have no fees, and there’s no minimum deposit required to get started.

If you want to invest and save at the same time, Public is a commission-free investing platform where individuals can build diversified portfolios, investing in assets like stocks, ETFs, and crypto — all with community support and real-time insights.

They also offer a high-yield cash account with competitive interest rates on uninvested funds, so that even your cash holdings see more growth over the long term.

This article provides information only and should not be construed as advice. It is provided without warranty of any kind.

Following the Federal Reserve’s recent 25-basis-point interest rate cut this month, homebuyers may be feeling a renewed sense of optimism. While lower mortgage rates are anticipated, housing prices may not necessarily follow suit.

However, Shark Tank’s Barbara Corcoran recently advised on Bloomberg Television that it’s prudent to start house hunting now to avoid increased competition from other buyers who may flood the market if rates continue to decline.

Lower mortgage rates would fuel “tremendous demand,” Shark Tank’s Barbara Corcoran told Bloomberg Television on Aug. 13. Her advice?

“I would say get out there,” she said. Because if rates continue to plummet, that will “bring everybody out into the market, and what’s going to happen is you’re going to pay more for [a] house.”

The state of the housing market

Consumer prices rose by 0.2% in October, according to the U.S. Bureau of Labor Statistics, bringing annual inflation to 2.6%, close to the Fed’s 2% target.

On Nov. 7, Fed Chair Jerome Powell announced the second rate cut this year, slashing the benchmark federal funds rate by 0.25%. And on November 12 the rate stayed the course. “Overall, [we’re] feeling good about economic activity,” Powell said during the post-meeting news conference last week.

It’s the kind of news that may give prospective homebuyers pause. If you’re in the market but aren’t sure if now is the right time because of a Fed rate in flux, you can seek advice from professionals through Advisor.com.

They offset the legwork of finding an advisor with their exclusive network of fiduciary advisors who offer personalized strategies.

With Advisor.com, advisors are held to high ethical standards, keeping your best interests front and center.

While rate cuts may not immediately lower mortgage rates, many experts expect they’ll boost housing demand, which could drive prices up. Freddie Mac noted that high mortgage rates had “led some prospective buyers to step back,” but a drop in rates could spark a “significant surge” in demand, especially from first-time buyers. They forecast home prices to increase by 2.1% in 2024 and 0.6% in 2025.

What can homebuyers do?

The starter home market is “crazy,” says Corcoran. “There’s so much competitive bidding, so much going over the price and so much fear going around because people feel like they can’t get ahead.” That’s why waiting to buy may not deliver the win you want.

“Wait until you see what happens with prices when interest rates come down another percentage point,” she told Bloomberg. If you are considering buying a new home, you need to know your options. Freddie Mac suggests getting mortgage quotes from three to five lenders. This will help you snag the best mortgage rate possible.

Borrowers who received two rate quotes saved up to $600 annually, according to 2023 research from Freddic Mac. That number rose to $1,200 annually for borrowers who visited at least four rate quotes from different lenders.

If you want a quick and efficient way to do this, Mortgage Refinance Center (MRC) can help you quickly compare rates and estimated monthly payments from multiple vetted lenders. All you have to do is enter some basic information about yourself, such as your zip code, your desired property type and price range and annual income.

Based on the information you provide, MRC will show you mortgage offers tailored to your needs so you can shop for a mortgage with confidence.

Sadly, we don’t all have the money to jump into the housing market at a specific time like when the Fed rate drops. If what Corcoran is hinting at turns out to be true, and lower rates catapult market demand all over again, companies like Cityfunds offer a smart alternative for those hesitant to jump into an overheated housing market.

As a real estate investment platform, Cityfunds allows individuals to invest directly in the future value of owner-occupied homes without needing to buy property outright. As these homes appreciate, your Cityfunds equity investment grows alongside the homeowner’s.

Operating in sought-after major markets like Austin, Dallas, Miami, Tampa, Denver, Phoenix, and Nashville, Cityfunds even offers the potential to invest in homes close to you. With a minimum investment of just $500, you can access the $20 trillion home equity market — bypassing steep home prices, costly mortgages, and the complexities of property ownership.

In a Fed rate-cutting cycle that could drive up demand and make real estate harder to attain, the Arrived Private Credit Fund is another alternative real estate investment that gets you in on the lending side of the building business.

This fund invests in supporting professional real estate projects, such as property renovations, rehabs, and new construction, all secured by residential housing. Loan periods range from 6 to 36 months, and returns are generated through monthly interest payments distributed directly to investors.

With a low minimum investment of $100, the fund has historically yielded 8.1% annualized dividends and aims to deliver 7-9% in cash returns. It features quarterly liquidity, a diversified pool of real estate-backed loans, and monthly dividend payouts, making it an attractive income-focused option with security from real estate collateral.

Determined homebuyers, on the other hand, have two choices: wait and try to time the market, or jump in now, endure short-term challenges, and potentially refinance if rates drop.

If you do end going the refinance route, Mortgage Research Center can also help you shop for a better rate.

Just answer a few quick questions about your current home and loan, and MRC will you show you rates from multiple lenders so you can make a decision with confidence.

For those who can afford it, entering the market before demand spikes might make sense. Rising home prices would build equity, and even if prices stay steady, there’s a better chance of landing a desired home without a buyer frenzy.

This article provides information only and should not be construed as advice. It is provided without warranty of any kind.

If you’re looking to buy a home in Canada in 2024, you might notice the housing market feels different from recent years. After a period of intense demand and skyrocketing prices, the real estate market is now experiencing a slowdown. Sales have declined in several regions, and prices are starting to ease in some areas, giving buyers a slight advantage that hasn’t been seen for a while. While the reductions aren’t drastic across the board, many cities are seeing more gradual price adjustments as the market stabilizes.

This cooling in the market comes as Canada tightens its immigration policies in response to concerns over housing affordability and infrastructure strain. However, with some Americans considering a relocation to Canada, demand from foreign buyers could still have a stabilizing effect on property prices. For the near future, these changes mean the housing market may see a complex interplay of factors as supply and demand shift.

Even so, for those who are budget-conscious, Canada’s diverse markets still offer some good options. Here’s an updated look at what $500,000 can get you in various Canadian cities — from cozy condos in urban centers to spacious family homes in more affordable regions.

Victoria, BC

BCHomegroup.ca | MLS

Based on recent 2024 data, housing prices in Victoria have continued to rise.

For $500,000, buyers are generally limited to smaller condos in the city. The average condo in central Victoria now costs around $525,000. In outlying areas like Hillside, $500,000 can typically secure a one-bedroom, one-bathroom unit of around 650 to 750 square feet, slightly smaller than previous years but still offering access to amenities and proximity to downtown.

As of 2024, the Vancouver housing market remains one of Canada’s most expensive.

For around $500,000, buyers are generally limited to micro-studios or very small one-bedroom units. In the downtown area, a $500,000 budget typically affords a studio apartment of 350 to 400 square feet with one bathroom. This size reduction reflects rising costs, even as the average condo price in the city exceeds $900,000.

Kelowna, BC

Realtor.ca | MLS

In 2024, the Kelowna market has seen significant appreciation.

A $500,000 budget now typically buys a two-bedroom, one-bathroom condo within city limits or a small cottage-style home in outlying areas. Properties offering lake access or scenic views are generally priced higher, making such amenities harder to find within this budget.

Calgary remains one of the more affordable large Canadian cities.

In 2024, a budget of $500,000 can typically secure a two to three-bedroom house with one to two bathrooms in suburban areas or a larger condo within the city. The typical square footage for this budget has increased slightly, offering 1,200 to 1,400 square feet depending on the neighbourhood.

Edmonton remains highly affordable in 2024 compared to other major cities.

For $500,000, buyers can find spacious single-family homes with three to four bedrooms and two to three bathrooms in established neighbourhoods or newer developments. Typical homes offer 1,800 to 2,200 square feet of living space, and suburban options often come with large yards.

In 2024, $500,000 remains a generous budget for Regina, SK.

Buyers in this price range can expect to find newer or recently updated single-family homes with three to four bedrooms and two to three bathrooms. Homes within city limits commonly provide around 1,600 to 1,900 square feet, often with large yards and modern finishes.

Saskatoon, SK

Realtor.ca | MLS

For $500,000 in 2024, buyers in Saskatoon, SK can still find spacious family homes, though options are typically three to four bedrooms and two to three bathrooms. Properties in this budget often provide 1,700 to 2,000 square feet in suburban areas, and many homes include modern amenities such as finished basements and open floor plans.

Winnipeg, MB

Realtor.ca | MLS

In Winnipeg, $500,000 in 2024 allows for a well-sized, detached home in established neighbourhoods or newer subdivisions.

Buyers can expect to find three to four-bedroom homes with two to three bathrooms and around 1,600 to 1,800 square feet. Many properties offer landscaped yards and proximity to parks and amenities, though premium features like pools are rare at this price point.

As of 2024, Toronto’s real estate market remains highly competitive.

For $500,000, buyers are generally limited to older or smaller condos, rather than townhouses, within the city. In neighbourhoods like West Humber, a $500,000 budget may secure a one-bedroom condo or a small two-bedroom unit with 600 to 750 square feet, often with limited updates.

In 2024, Mississauga’s housing market remains robust.

For $500,000, buyers can generally afford a one-bedroom condo or a smaller two-bedroom unit of around 700 to 850 square feet. Condos in this range may include access to amenities like gyms and shared outdoor spaces, though outdoor private patios are less common.

In Ottawa, $500,000 in 2024 can generally afford buyers a two-bedroom townhouse or a one-bedroom condo closer to the city center. Townhouses in outlying areas like Rockland offer around 1,100 to 1,300 square feet, while condos in central Ottawa average around 700 to 850 square feet.

Kitchener, ON

Realtor.ca | MLS

The 2024 market in Kitchener is competitive due to its proximity to Waterloo’s tech sector.

For $500,000, buyers can generally find two-bedroom condos or smaller semi-detached homes with around 850 to 1,100 square feet. Detached homes in this range are rare and tend to be smaller with modest updates.

Montreal, QC

Realtor.ca | MLS

In 2024, $500,000 remains sufficient for newer condos in Montreal’s suburbs, such as Longueuil. Buyers in this price range can expect two-bedroom units with 850 to 1,000 square feet. Within Montreal proper, similarly priced units are typically smaller, one-bedroom condos or older units in established neighbourhoods.

Quebec City

Realtor.ca | MLS

In 2024, Quebec City remains relatively affordable.

A budget of $500,000 can often secure a three to four-bedroom home with two bathrooms, offering around 1,800 to 2,000 square feet. Properties are generally newer or updated, with spacious layouts and ample natural light. However, five-bedroom homes are now rare in this range due to slight increases in the local housing market.

Saint John, NB

Realtor.ca | MLS

Saint John remains one of Canada’s most affordable markets.

In 2024, $500,000 can secure a large historic home or a newer property with three to four bedrooms, two to three bathrooms, and approximately 2,000 to 2,500 square feet. While 6,500-square-foot homes are rare in this price range, buyers still have options for spacious properties, especially in older neighbourhoods.

Moncton, NB

Realtor.ca | MLS

In Moncton, $500,000 remains a substantial budget in 2024. Buyers can typically find spacious homes with three to four bedrooms, two to three bathrooms, and 2,000 to 2,500 square feet of space. Such homes often include updated kitchens and landscaped yards. However, five-bedroom properties are now rare in this budget.

Fredericton, NB

Realtor.ca | MLS

Fredericton remains affordable in 2024.

A $500,000 budget can typically secure a three-bedroom, two-bathroom home with 1,600 to 1,800 square feet in newer suburban developments or established neighbourhoods. These homes often feature modern amenities, including hardwood floors and open floor plans.

Halifax, NS

Realtor.ca | MLS

In 2024, Halifax continues to offer investment opportunities within the $500,000 budget. Buyers can often find duplexes or single-family homes with potential for rental income. Typical properties include two to three bedrooms with one to two bathrooms per unit, offering around 1,400 to 1,600 square feet. Rental demand remains high due to the city’s growing population.

Charlottetown, PEI

Realtor.ca | MLS

Charlottetown remains one of Canada’s more affordable markets.

In 2024, with a $500,000 budget, buyers can secure a sizable single-family home with three to four bedrooms and two bathrooms, usually between 1,800 to 2,200 square feet. Properties in this range often include larger lots and are located in well-established neighbourhoods.

St. John’s, NL

Realtor.ca | MLS

In St. John’s, $500,000 is still considered a high-end budget in 2024. For this price, buyers can often secure three to four-bedroom homes with two to three bathrooms, around 2,000 to 2,400 square feet. Properties within this budget are typically newer and located in desirable neighbourhoods with easy access to amenities.

*Sources: Realtors Association of Edmonton (RAE), Association of Saskatchewan REALTORS® (ASR), Saskatoon Region Association of REALTORS® (SRAR), Winnipeg Real Estate Board (WREB), Toronto Regional Real Estate Board (TRREB), Mississauga Real Estate Board (MREB), Ottawa Real Estate Board (OREB), Kitchener-Waterloo Association of REALTORS® (KWAR), Quebec Professional Association of Real Estate Brokers (QPAREB), Saint John Real Estate Board Greater Moncton REALTORS® du Grand Moncton, Real Estate Board of the Fredericton Area, Nova Scotia Association of REALTORS® (NSAR), Prince Edward Island Real Estate Association (PEIREA), Newfoundland and Labrador Association of REALTORS® (NLAR), Canada Mortgage and Housing Corporation (CMHC), Canadian Real Estate Association (CREA), Statistics Canada: Housing Market Data

Disclosure: This content was generated with the assistance of AI technology. While the information and insights provided aim to be accurate and engaging, please keep in mind that the final content was influenced by AI-driven tools. For specific advice or decisions, always consult a financial professional or trusted expert.

Based on recent 2024 data, housing prices in Victoria have continued to rise.

For $500,000, buyers are generally limited to smaller condos in the city. The average condo in central Victoria now costs around $525,000. In outlying areas like Hillside, $500,000 can typically secure a one-bedroom, one-bathroom unit of around 650 to 750 square feet, slightly smaller than previous years but still offering access to amenities and proximity to downtown.

As of 2024, the Vancouver housing market remains one of Canada’s most expensive.

For around $500,000, buyers are generally limited to micro-studios or very small one-bedroom units. In the downtown area, a $500,000 budget typically affords a studio apartment of 350 to 400 square feet with one bathroom. This size reduction reflects rising costs, even as the average condo price in the city exceeds $900,000.

Kelowna, BC

Realtor.ca | MLS

In 2024, the Kelowna market has seen significant appreciation.

A $500,000 budget now typically buys a two-bedroom, one-bathroom condo within city limits or a small cottage-style home in outlying areas. Properties offering lake access or scenic views are generally priced higher, making such amenities harder to find within this budget.

Calgary remains one of the more affordable large Canadian cities.

In 2024, a budget of $500,000 can typically secure a two to three-bedroom house with one to two bathrooms in suburban areas or a larger condo within the city. The typical square footage for this budget has increased slightly, offering 1,200 to 1,400 square feet depending on the neighbourhood.

Edmonton remains highly affordable in 2024 compared to other major cities.

For $500,000, buyers can find spacious single-family homes with three to four bedrooms and two to three bathrooms in established neighbourhoods or newer developments. Typical homes offer 1,800 to 2,200 square feet of living space, and suburban options often come with large yards.

In 2024, $500,000 remains a generous budget for Regina, SK.

Buyers in this price range can expect to find newer or recently updated single-family homes with three to four bedrooms and two to three bathrooms. Homes within city limits commonly provide around 1,600 to 1,900 square feet, often with large yards and modern finishes.

Saskatoon, SK

Realtor.ca | MLS

For $500,000 in 2024, buyers in Saskatoon, SK can still find spacious family homes, though options are typically three to four bedrooms and two to three bathrooms. Properties in this budget often provide 1,700 to 2,000 square feet in suburban areas, and many homes include modern amenities such as finished basements and open floor plans.

Winnipeg, MB

Realtor.ca | MLS

In Winnipeg, $500,000 in 2024 allows for a well-sized, detached home in established neighbourhoods or newer subdivisions.

Buyers can expect to find three to four-bedroom homes with two to three bathrooms and around 1,600 to 1,800 square feet. Many properties offer landscaped yards and proximity to parks and amenities, though premium features like pools are rare at this price point.

As of 2024, Toronto’s real estate market remains highly competitive.

For $500,000, buyers are generally limited to older or smaller condos, rather than townhouses, within the city. In neighbourhoods like West Humber, a $500,000 budget may secure a one-bedroom condo or a small two-bedroom unit with 600 to 750 square feet, often with limited updates.

In 2024, Mississauga’s housing market remains robust.

For $500,000, buyers can generally afford a one-bedroom condo or a smaller two-bedroom unit of around 700 to 850 square feet. Condos in this range may include access to amenities like gyms and shared outdoor spaces, though outdoor private patios are less common.

In Ottawa, $500,000 in 2024 can generally afford buyers a two-bedroom townhouse or a one-bedroom condo closer to the city center. Townhouses in outlying areas like Rockland offer around 1,100 to 1,300 square feet, while condos in central Ottawa average around 700 to 850 square feet.

Kitchener, ON

Realtor.ca | MLS

The 2024 market in Kitchener is competitive due to its proximity to Waterloo’s tech sector.

For $500,000, buyers can generally find two-bedroom condos or smaller semi-detached homes with around 850 to 1,100 square feet. Detached homes in this range are rare and tend to be smaller with modest updates.

Montreal, QC

Realtor.ca | MLS

In 2024, $500,000 remains sufficient for newer condos in Montreal’s suburbs, such as Longueuil. Buyers in this price range can expect two-bedroom units with 850 to 1,000 square feet. Within Montreal proper, similarly priced units are typically smaller, one-bedroom condos or older units in established neighbourhoods.

Quebec City

Realtor.ca | MLS

In 2024, Quebec City remains relatively affordable.

A budget of $500,000 can often secure a three to four-bedroom home with two bathrooms, offering around 1,800 to 2,000 square feet. Properties are generally newer or updated, with spacious layouts and ample natural light. However, five-bedroom homes are now rare in this range due to slight increases in the local housing market.

Saint John, NB

Realtor.ca | MLS

Saint John remains one of Canada’s most affordable markets.

In 2024, $500,000 can secure a large historic home or a newer property with three to four bedrooms, two to three bathrooms, and approximately 2,000 to 2,500 square feet. While 6,500-square-foot homes are rare in this price range, buyers still have options for spacious properties, especially in older neighbourhoods.

Moncton, NB

Realtor.ca | MLS

In Moncton, $500,000 remains a substantial budget in 2024. Buyers can typically find spacious homes with three to four bedrooms, two to three bathrooms, and 2,000 to 2,500 square feet of space. Such homes often include updated kitchens and landscaped yards. However, five-bedroom properties are now rare in this budget.

Fredericton, NB

Realtor.ca | MLS

Fredericton remains affordable in 2024.

A $500,000 budget can typically secure a three-bedroom, two-bathroom home with 1,600 to 1,800 square feet in newer suburban developments or established neighbourhoods. These homes often feature modern amenities, including hardwood floors and open floor plans.

Halifax, NS

Realtor.ca | MLS

In 2024, Halifax continues to offer investment opportunities within the $500,000 budget. Buyers can often find duplexes or single-family homes with potential for rental income. Typical properties include two to three bedrooms with one to two bathrooms per unit, offering around 1,400 to 1,600 square feet. Rental demand remains high due to the city’s growing population.

Charlottetown, PEI

Realtor.ca | MLS

Charlottetown remains one of Canada’s more affordable markets.

In 2024, with a $500,000 budget, buyers can secure a sizable single-family home with three to four bedrooms and two bathrooms, usually between 1,800 to 2,200 square feet. Properties in this range often include larger lots and are located in well-established neighbourhoods.

St. John’s, NL

Realtor.ca | MLS

In St. John’s, $500,000 is still considered a high-end budget in 2024. For this price, buyers can often secure three to four-bedroom homes with two to three bathrooms, around 2,000 to 2,400 square feet. Properties within this budget are typically newer and located in desirable neighbourhoods with easy access to amenities.

*Sources: Realtors Association of Edmonton (RAE), Association of Saskatchewan REALTORS® (ASR), Saskatoon Region Association of REALTORS® (SRAR), Winnipeg Real Estate Board (WREB), Toronto Regional Real Estate Board (TRREB), Mississauga Real Estate Board (MREB), Ottawa Real Estate Board (OREB), Kitchener-Waterloo Association of REALTORS® (KWAR), Quebec Professional Association of Real Estate Brokers (QPAREB), Saint John Real Estate Board Greater Moncton REALTORS® du Grand Moncton, Real Estate Board of the Fredericton Area, Nova Scotia Association of REALTORS® (NSAR), Prince Edward Island Real Estate Association (PEIREA), Newfoundland and Labrador Association of REALTORS® (NLAR), Canada Mortgage and Housing Corporation (CMHC), Canadian Real Estate Association (CREA), Statistics Canada: Housing Market Data

Disclosure: This content was generated with the assistance of AI technology. While the information and insights provided aim to be accurate and engaging, please keep in mind that the final content was influenced by AI-driven tools. For specific advice or decisions, always consult a financial professional or trusted expert.

If you’re one of the projected 430,000 to 542,000 people who have immigrated to Canada this year, welcome! Aside from acclimating yourself to a new country, home and job, you’ll also quickly realize the benefits of building a credit history with a strong credit score.

Whether you’re looking to lease a car or buy a home, you’re going to want to start building a credit history right away to get access to lending products at the best rates available. Here are a few tips to help you get started.

Why you need to build up credit

In Canada, lenders report the relevant details of your credit accounts (whether you’re paying on time, how much of a balance you carry and more) to two major credit bureaus: Equifax and TransUnion.

From there, the credit bureaus give you a three-digit score between 300 and 900.

Most of the time, you’ll need a credit score to:

Rent an apartment or buy a house

Take out credit cards

Take out a private student loan

Apply for a job

Get utilities to connect to your home

Get a cellphone

How to build up your credit

First of all, you want to get an idea of how far you need to go to qualify for better interest rates or become a better borrower. Fortunately, you can check your score for free online.

Now that you know your baseline, remember there are five factors that go into calculating your credit score. While your payment history and level of debt carry a lot of weight, there’s also how long you’ve had your credit accounts, what mix of credit you carry and how many new accounts you have.

With that in mind, here are five of the best ways to build up your credit as an immigrant to Canada looking to build a healthy financial profile.

Apply for an unsecured credit card: Apply for a Canadian credit card as soon as possible. Many of the big banks offer new immigrants a credit card with a low line of credit as part of their initial banking package, including RBC’s “Welcome to Canada” package or Scotiabank’s “Start Right” program. Once you get your credit card, start using it right away.

Apply for a secured card if need be. Not everyone will be eligible for an unsecured credit card without credit history. Those who find themselves in this position should instead consider applying for a secured credit card, which requires a refundable security deposit (typically matching the card’s credit limit). The advantage of using a secured card is that your repayment habits will be reported to the credit bureaus, allowing you to gradually build the all-important credit history you need.

Apply for a mobile phone. Some phone carriers, such as Telus, specifically state that no credit history is required to get an account, and that they will report your post-paid subscription to the credit bureaus. While you may be tempted to get a pre-paid plan, a post-paid plan will help you build a credit history.

Pay your credit card bill on time. Whether paying the minimum or more, make your credit card bill payments on or before the due date. Thirty-five percent of your credit score is based on payment history. If you’re late, even by an hour, your credit history will be negatively impacted. Paying on time does not mean paying your entire balance. Paying on time means paying the monthly minimum payment at the very least, which is shown on your credit card statement. Understand how long you have after receiving your credit card bill to make your payment, which is called the "grace period" — it’s usually around 21 days. To help you pay on time, you can set-up automatic monthly payments through your bank account.

Pay off your balance in full each month. While carrying a balance and making your payments on time will help your credit history more than paying in full each month, we would never recommend carrying a balance just to build your score. This is actually a myth when it comes to what affects your credit score, so be careful with your balance. Using your credit card and paying it off every month will help build your credit score as well, just not as fast. However, it’s a better strategy than paying excessive interest charges just to build a credit history.

Get different types of credit. The credit bureaus love people with different sources of credit. So if you can manage to get a credit card, cell phone, or car loan (usually with a large deposit), it will help you build a credit history with a strong score that much faster.

Build your credit score with some help. Use tools to help you build your credit score faster. If money is tight, consider a free tool although the options for real-time tracking and personalized insight may be limited. If you have a bit of funds to commit to building a credit score, consider paying for a tool that helps you track and improve your credit history using personlized recommendations.

Financial institutions will usually start using your credit history after it’s been established in good standing for a period of 18 months. But several other factors will be considered as well, including your savings history, net worth, income and ability to provide a security deposit — such as a down payment on a mortgage. These strategies should go a long way towards establishing a Canadian credit history for new immigrants.

Sources

1. Government of Canada: Immigration, Refugees and Citizenship Canada Departmental Plan 2023-2024

We are alone but we are many. We are single-income, single parents paying a premium to pay bills and buy necessities for our smaller-sized households. We feel that pinch.

Step into a Costco and you’ll know how much cheaper (on a per unit basis) it is to buy bulk. But for many households, like mine, there aren’t enough people under the roof to make these purchases realistic. We will never finish that vat of mayo nor do I have the space in my humble home to store that skid of toilet paper.

It’s not just the bulk-is-better marketing. Add in the tax breaks and admission incentives and the argument gets stronger: the economy is set up in such a way as to benefit larger families — nuclear, blended or multi-generational.

As a single parent, I pay a premium to supply and care for my small family. I feel the impact on my budget because I can’t take advantage of the savings of buying bulk. It’s only my paycheque paying the bills. It’s only me determining when to buy and when to wait. Let’s face it: single folk, especially those with children, just pay more.

So are businesses missing out on converting this large segment of people into loyal customers? This single-income, single-parent household says: yes, most definitely.

Missing out on a loyal customer by ignoring the single-income household

We single-income households make up a strong portion of the purchasing public, it makes good business sense to speak directly to us and cater to our unique needs. We make purchasing decisions based not just on the hard numbers, but there are emotional and psychological reasons we choose things, too.

There are almost 1.1 million single-income households in Canada, according to the latest statistics from 2022. These households get by on a median income of $43,590. Of those households, just shy of 42% have two or more children.

That’s a lot of solo decision-makers across this country — many of whom have dependents — for business to ignore.

Want my money? Appeal to my head…and my heart

Solo-income families tackle two realities when faced with a purchase decision: Can we justify the expense? And, does it make sense based on our single-income budget?

While logic dictates many of these decisions, our heads and hearts play a large factor. Understanding that we buy with our head as well as our heart is good business for companies looking to expand their market.

Amrit Richmond of Medium, a digital marketing publication, explains that a lot goes into purchasing decisions. There are the basics — cost, colour and quality, as well as personal experience or consumer testimonials — such as solid reviews, featured articles and product safety, among various other factors.

“In today’s economy, consumers have multiple choices for pretty much everything: coconut water, sneakers, airlines, and cell phones,” Richmond says. “Consumers are increasingly curious and conscious of your ingredients, labour practices, and competitors.”

Every buying decision I make is weighing needs against wants and cost against value. And value isn’t just about the hard numbers. With so many companies competing on price, understanding what single income homes value is a competitive edge they should consider.

Single-income families need to buy things, too

Furnishing my first home post-separation, and buying food and clothes for myself and my children, most certainly involves a myriad of emotions, every time I shop.

Now that you know we are out there, in large numbers, wanting to buy and needing to buy, businesses also need to recognize that we can and will buy.

The reality is that every household needs to buy things. Single-income households have the same needs, but our means are different.

This is particularly true of households with growing children. As a single mom with young teenagers, all expenses take a significant bite out of my wallet.

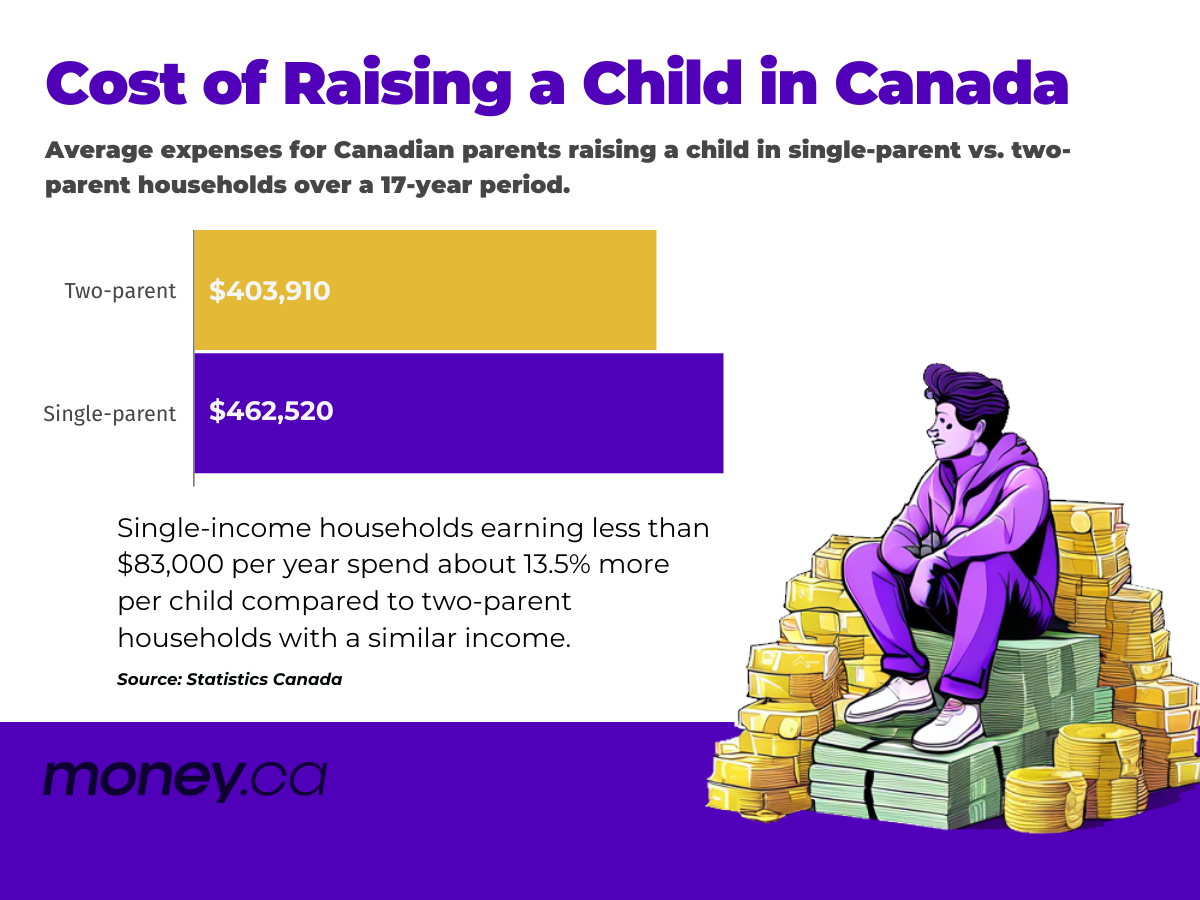

The real cost of raising a family

According to Statistics Canada, the cost to raise a child from birth to age 17 is just over $290,000 — for each child! That means the average child costs $17,000 per year — but only if the child lives in a household with two parents. Simple math suggests that each earner is responsible for about $8,500 in child-related expenses per year.

For one-parent families, the average annual expenditure on each child is closer to $13,500. Again, simple math suggests that the single-income earner pays more than 45% more, per child per year.

And that’s just until age 17. As we know most kids don’t leave home, let alone for good, when they graduate from high school.

Money.ca

We talk, so you better start listening

I’ve already explained how consumers buy (with emotion!) and I don’t have to tell you that choosing a couch for your living room is based on more than the price tag: Will it physically fit in the space? Will it be able to endure my children? Do I want to pay more now for better quality so that it lasts longer? Will my budget even allow that?

Chances are better than not I’m going to turn to my single-mom network and ask for recommendations on where I can get the best bang for my buck to furnish my space. Companies that realize the value we provide are more likely to come up when I seek this input. If you market to us, we will recommend you!

Putting a price on loyalty

Research conducted by the Harvard Business Review found that companies that focus on the value of Net Promoter Scores (a fancy way of saying the people who recommend or vouch for you) tend to reap the rewards in their bottom line.

“Loyalty leaders — companies at the top of their industries in Net Promoter Scores or satisfaction rankings for three or more years — grow revenues roughly 2.5 times as fast as their industry peers and deliver two to five times the shareholder returns over the next 10 years,” the study found.

“Yet companies and investors continue to prioritize quarterly earnings over customer relationships.”

Let’s take a look at an example of a company that did just that.

Think outside of the box

About 20 years ago, the largest condo developer Tridel began to focus on single women as homebuyers — and it paid off.

Back in 2013, Jim Ritchie, senior vice president of sales and marketing for Tridelsaid single women accounted for one-third of all new sales. That’s a rather large chunk.

In fact, at the time, the Globe and Mail said young single women were becoming a ‘dominant force’ in the condo market and that developers who acknowledged that were shifting their focus to cater to them.

“Developers have taken note, and are responding by designing buildings and individual units to suit their tastes and interests, whether it’s improving the quality of lighting, or installing security cameras in parking garages, or creating floor plans that maximize storage space.”

Tridel understood what bulk buying costs fail to: Maximizing space storage is a key factor for families and bulk buying definitely does not fit into that neat little package.

Value the undervalued

The 2016 census showed that in the year previous, working women earned an average annual salary of $35,461, compared to men who earned an average annual salary of $48,059. Do you know what that means to women bidding on homes? We lose out to men who are better able to afford them.

Detached housing, in general, does not support the needs of single-income homes, with kids or without. They were built with families in mind, who needed space and have better means (i.e. two incomes) to afford it.

In 2021, the Walrus wrote an article speaking to the challenges faced by a single woman’s ability to live in post-war-build communities, such as the Etobicoke suburb of Thorncrest Village. This area, in particular, was built exclusively for detached housing. When speaking about the community, Marshall Foss, the neighbourhood’s lead developer, described Thorncrest’s layout as an asset that ensured “your property values and your living values are secure and stabilized.”

For whom, though? Two-parent, two-income families..

Families come in many forms

But what of single women?

“While policy preference for single-family housing was established with the nuclear family in mind, it did not respond to the complexities of the female experience,” write the author of that 2021 Walrus article.

“Because the zoning effectively prioritized the development of single-family housing, as opposed to housing affordability, the social networks of divorced women were weakened because the neighbourhoods where they lived during their marriages did not offer an adequate supply of housing affordable to them when they became single.”

These women had nowhere to go in their own communities when they became single. It simply was not built for them.

Thankfully, today, the federal government is acknowledging that single women need better accessibility to housing in Canada.

In a 2021 report released by the CMHC , the federal government said it aims to allocate 33% of the National Housing Strategy’s investments, with a minimum of 25% towards serving the unique needs of women and their children. Further, the report acknowledged that women are more likely to be lone parents than men (13.2% compared to 9.6%).

In other words, the government understands that it’s hard to live on one income, especially for women, who make less on the dollar than their male counterparts and are more likely to be single parents.

Businesses should take the government’s lead.

It’s because my money needs to be spent in order to provide for myself and my family. We need a place to live. We need food on our plates and yes, mayo on my sandwiches and toilet paper in the bathroom. I have an income and buying power. And I am but one, of many just like me, who struggles with paying more for less, when my needs are more and my means are less.

It’s not just because we are many. It’s not just because we have needs, too. It’s not even because it’s good for business.

When you think of Tony Hawk, chances are you picture him pulling off a 900 or flying high in a skatepark. But beyond his legendary skateboarding skills, Tony Hawk’s financial success offers some valuable lessons for investors. Not only did the Hawk conquer the skateboarding world, but along the way he learned a few savvy financial moves that investors of all levels can learn from.

In a YouTube video, the old-school skater chats with hosts of Nine Club Clips to reveal what he learned about finance and the power of money as he built his brand and his business.

Here are three key lessons investors can learn from Tony Hawk’s journey to financial success.

#1. Unexpected success can be life-changing—if you’re ready for it

Tony Hawk’s Pro Skater video game series was a massive hit, but even Hawk himself didn’t anticipate just how successful it would become. After the release of the fourth game in the series, he was shocked to learn that the first three games were still in the top 10 sales. The result? A surprise USD$4 million royalty cheque that changed his life.

What’s the takeaway for investors? Be ready to seize opportunities. Sometimes, a single investment or venture can unexpectedly take off, offering life-changing financial rewards. But this only happens if you’re in the right place at the right time, with the right mindset, to take advantage of the opportunity. Like Hawk, it’s important to diversify your efforts and be prepared to reinvest in your future when success comes knocking.

#2. Importance of giving back

Hawk didn’t just sit on his newfound wealth. He used a significant portion of his earnings to give back through his Tony Hawk Foundation, which builds skateparks in underprivileged areas. This not only helps young skaters have a safe place to practice, but also contributes to communities that often lack recreational facilities.

What’s the takeaway for investors? Despite success, Hawk’s experience highlights the importance of reinvesting in your community and supporting causes you care about. Philanthropy can be a powerful way to share your success, and it also builds a lasting legacy. Whether donating a portion of your earnings to charity, investing in sustainable businesses, or supporting local initiatives, giving back can create a ripple effect beyond financial returns.

#3. Staying humble even in success

Despite his wealth and fame, Tony Hawk is known for staying grounded. He doesn’t flaunt his success, preferring to focus on meaningful projects and personal fulfillment rather than flashy displays of wealth. Hawk’s humility is a reminder that staying grounded is key to long-term success.

What’s the takeaway for investors? It can be easy to get caught up in chasing profits and showing off when things are going well. However, staying humble, avoiding risky or showy investments, and keeping your focus on long-term goals can help you sustain your financial success. True wealth isn’t just about money — it’s about how you use it and how it aligns with your values.

Tony Hawk’s investment strategy

Tony Hawk’s approach to investing is another area where he offers valuable lessons. Here’s how he’s diversified his wealth and how investors can follow suit:

Real estate

Hawk has invested in a mix of residential and business properties. Real estate is a tried-and-true investment strategy, offering steady income and long-term appreciation. Whether you’re buying your first rental property or expanding into commercial spaces, it’s a smart way to build wealth over time.

Philanthropy

As mentioned, Hawk has dedicated a portion of his income to philanthropy through his foundation. Beyond personal fulfillment, charitable giving can have tax advantages and can be an integral part of estate planning for those thinking long-term.

Business ventures

Hawk has invested in multiple business ventures, including his skateboard company Birdhouse and various clothing and video game projects. For investors, this highlights the importance of staying connected to your passions. By backing businesses that align with his personal interests, Hawk has been able to stay engaged and motivated.

Stocks and private equity

Finally, Hawk has also diversified into stocks and private equity investments, putting money into tech companies and startups. Diversifying your investment portfolio beyond a single asset class can help mitigate risk and open up new growth opportunities, whether it’s through stocks, bonds, or venture capital.

To start investing im equities, you’ll need to open a direct brokerage account. Open a CIBC Investor’s Edge account before March 31, 2025 and you can start building your own investment portfolio using the mobile app or online trading platform, plus get 100 free trades when you open a CIBC Investor’s Edge account using promo code EDGE2425.

Bottom line

Tony Hawk’s journey from professional skateboarder to savvy investor is full of valuable lessons. Whether it’s being prepared for unexpected success, giving back to the community, staying humble, or diversifying your investments, Hawk’s approach is one we can all learn from. His story proves that the principles of success — whether in skateboarding, business, or investing — often overlap. So, as you roll toward your own financial goals, remember to take a few tips from the “Birdman” himself!

Sources

1. Nine Club Clips: How Much Money Did Tony Hawk Make From Tony Hawk’s Pro Skater?? (June 15, 2018)

Countless Americans are chasing the dream of one day becoming rich. But at some point in the race, many of them come to find there’s an important difference between being rich and feeling rich.

Let’s say you’re a surgeon, married, in your late 40s and your household brings in a tidy $573,000 each year. Considering that the median income in the U.S. was $75,149 between 2018 and 2022 — based on U.S. Census Bureau data — you’re doing pretty good. More than good.

At this point, you shouldn’t feel broke — especially if you’re working with a financial adviser who should be helping you to make smart decisions to use all that money as wisely as possible.

But if you are struggling, it’s worth looking at whether your adviser could be doing you a disservice, either by steering you in the wrong direction or by charging you unreasonable fees.

Not all financial advisers are created equal

Whenever you place your finances in the hands of someone else, you take a risk — but the risk is greater with certain kinds of advisers.

First and foremost, if your adviser isn’t a fiduciary, you could have a problem. A fiduciary has a legal duty to act in your best interest and give you advice that’s right for you. Someone who is not a fiduciary doesn’t have the same strong legal obligations.

It may come as a surprise, but not all people who bill themselves as financial advisers have fiduciary status. Some professionals, like Certified Financial Planners, are held to a fiduciary standard but many individuals can offer financial advice even if they don’t have this special designation.

You’ll also want to see what licensing your adviser has. Ideally, you’ll want someone with independent certification, such as a CFP or a chartered financial analyst. Advisers who are licensed by independent agencies are typically held to higher ethical standards and have had to undergo specialized training and complete exams.

Finally, you’ll want to find out how your adviser charges. If they work on commission, this can create a conflict of interest because they may be tempted to steer you into investments that earn them the most money even when those investments aren’t actually the best ones for you.

Your adviser will ideally be fee-only and will charge you a predetermined, agreed-upon fee for managing your assets. AdvisoryHQ reports that the average adviser fee for someone with $1 million in assets came in at around 1.02% in 2023. If your adviser is charging much more than that, their fee structure may be unfair.

What to do if you suspect your financial adviser is ripping you off

If you’re concerned about whether your adviser is ripping you off, ask to see your account statements, a summary of your transactions, and a summary of what you’ve paid to your adviser. You should also ask them if they’re acting as a fiduciary.

If they say they aren’t a fiduciary, then at a minimum you should change advisers to one who is. If they’re unwilling to provide the documents you’re asking for, this is a major red flag and you may want to get legal help to recover your records and potentially take action if fraud is found.

Once you have your financial details in front of you, review the information carefully to see where your money is going, what fees you’re paying, and what ROI you’ve earned. Ask any questions you have to get to the bottom of why you don’t feel rich when you’re making so much.

Ultimately, whether it’s lifestyle decisions you’ve made or bad investments, you should have plenty of money to save, grow your wealth and live a comfortable life on an income of $573,000. If you aren’t doing that now, consider looking for a different licensed, fee-only adviser who can help you make a better plan for your financial future.

This article provides information only and should not be construed as advice. It is provided without warranty of any kind.

We adhere to strict standards of editorial integrity to help you make decisions with confidence. Some or all links contained within this article are paid links.

Between 1964 and 2023, his company, Berkshire Hathaway, achieved an astonishing total return of 4,384,748%.

In an interview at Georgetown University, an audience member cut to the chase, asking, “What would you think is the most important thing — the key — in evaluating a company?”

Without missing a beat, Buffett responded, “The most important thing is to be able to define which ones you can come to an intelligent decision on and which ones are beyond your capacity to evaluate.”

Buffett emphasized that you don’t need to understand — or be right about — thousands of companies to succeed. Instead, as he put it, you only need to be right about “a couple.”

To illustrate his approach, Buffett shared a memorable exchange with Microsoft co-founder Bill Gates.

When Gates tried to convince Buffett to enter the computer age

On July 5, 1991, Buffett and Gates were in Seattle when Gates, eager to share his enthusiasm for the burgeoning world of computers, turned to Buffett and said, “You’ve got to have a computer.”

“Why?” Buffett asked.

Gates replied with a practical suggestion, “Well, you can do your income tax on it.”

But Buffett, whose approach to wealth focused on reinvesting rather than receiving income, responded matter-of-factly, “I don’t have any income. Berkshire doesn’t pay a dividend.”

Gates pressed on, suggesting that a computer could help Buffett keep track of his stock portfolio. But Buffett, whose investment portfolio consisted solely of Berkshire Hathaway, simply responded, “I only have one stock.”

Undeterred, Gates insisted, “It’s going to change everything.”

This prompted Buffett to dig deeper. “Will it change whether people chew gum?” he asked.

“Probably not,” Gates admitted.

“Will it change what kind of gum they chew?” Buffett followed up, prompting Gates to again reply, “Nah.”

With that, Buffett summed up his thoughts: “Well, then I’ll stick to chewing gum and you stick to computers.”

Buffett used this story to highlight his investment philosophy. His success didn’t stem from understanding every emerging technology or industry trend; rather, it came from staying within his “circle of competence.”

In his view, you don’t need to know everything about every industry to succeed as an investor — you just need to thoroughly understand a few.

Billions in gum and soda

Chewing gum firmly falls within Warren Buffett’s “circle of competence.” In his 1993 letter to shareholders, Buffett identified Wrigley as “dominant” in the chewing gum market.

When food giant Mars sought to acquire Wrigley in 2008, Warren Buffett invested $6.5 billion — buying $2.1 billion of Wrigley preferred stock and $4.4 billion of its bonds — to help fund the deal.

The bet paid off handsomely: between interest payments, dividends, and gains on the bonds and shares, Buffett reportedly made an estimated $6.5 billion from his Wrigley investment.

Beyond chewing gum, Buffett has long been a fan of another staple: soda. Coca-Cola, a brand that’s been around since 1886, captured Buffett’s attention because of its vast market presence.

“Coca-Cola’s been around since 1886. There’s 1.8 billion 8-ounce servings of Coca-Cola products sold everyday now. If you get one penny extra — that’s $18 million a day, and $18 million times 365 is $6.57 billion annually… from one penny. Do you think Coca-Cola is worth a penny more than, you know, Joe’s Cola? I think so,” he explained.

True to his investment philosophy, Buffett’s conviction in Coca-Cola has stood the test of time. Berkshire first invested in Coca-Cola in 1988, and today, it holds 400 million shares of Coca-Cola, a stake now valued at $26 billion.

As we approach 2025, with the world growing more complex — marked by political uncertainty, economic pressures, global tensions and a rapidly evolving tech landscape — Buffett’s straightforward investment philosophy stands firm and relevant.

His approach reminds us that we don’t need to chase the latest trends to find success. Instead, Buffett advocates focusing on one’s circle of competence, sticking to businesses that are easy to understand and have enduring demand.

Rather than constantly predicting “the next big thing,” Buffett finds long-term value in companies with proven, lasting appeal.

It’s also easier than ever to start investing. Trading apps like Public allow everyday investors to capitalize on the stock market by investing in fractional shares for as little as $10. You can easily pack your portfolio with your favorite companies, with zero commissions.

To make informed decisions within your circle of competence, investors can use research tools like Moby, which provide expert analysis and market insights, helping users optimize their portfolios.

‘The best thing to do’

While Buffett is legendary for picking winning companies, he’s an even bigger advocate for a simpler, tried-and-true strategy: investing in an S&P 500 index fund.

“In my view, for most people, the best thing to do is own the S&P 500 index fund,” he famously stated. This straightforward approach gives investors exposure to 500 of America’s largest companies across various industries, providing diversified exposure without the need for constant monitoring or active trading.

Buffett believes so strongly in this strategy that he has instructed 90% of his wife’s inheritance be invested in “a very low-cost S&P 500 index fund” after he dies.

The beauty of this approach is its accessibility — anyone, regardless of wealth, can take advantage of it. Even small amounts can grow over time with tools like Acorns, a popular app that automatically invests your spare change.

Signing up for Acorns takes just minutes: link your cards, and Acorns will round up each purchase to the nearest dollar, investing the difference — your spare change — into a diversified portfolio. With Acorns, you can invest in an S&P 500 ETF with as little as $5 — and, if you sign up today, Acorns will add a $20 bonus to help you begin your investment journey.

This article provides information only and should not be construed as advice. It is provided without warranty of any kind.

Following Donald Trump’s election victory, financial markets experienced a flurry of trading activity, with investors increasingly turning to Bitcoin as a hedge amid heightened political uncertainty.

In Canada, more cautious investors turned to Bitcoin and cryptocurrency exchange-traded funds (ETFs). These ETFs accessibility and security within a regulated environment and, as a result, surged in popularity in the last few years as an entry into the cryptocurrency world. While Bitcoin ETFs and cryptocurrency funds make it easier to participate in cryptocurrency investments, potential investors should consider both the advantages and risks associated with this type of investment.

Why Bitcoin ETFs are drawing more Canadian investors

Bitcoin ETFs offer Canadians a straightforward way to gain exposure to Bitcoin’s price fluctuations without directly purchasing or holding the cryptocurrency. Traded on stock exchanges, these ETFs allow individuals to buy and sell shares much like traditional stocks, including within tax-advantaged accounts like TFSAs or RRSPs. This appeal is especially relevant now, as more investors seek assets tied to Bitcoin’s performance.

In response to this demand, Canadian firms like Purpose Investments have crafted Bitcoin ETFs with an emphasis on security. Purpose’s Bitcoin ETF, for example, employs “cold storage” — keeping Bitcoin assets offline to lower the risk of cyber attacks. This setup adheres to Canadian regulatory standards, offering investors additional safeguards typically absent in direct cryptocurrency purchases.

Benefits of Bitcoin ETFs: Combining accessibility with security

Bitcoin ETFs make crypto investment easier by eliminating the need for private wallets and technical knowledge, while also simplifying asset security. With Canadian regulatory oversight, these ETFs come with protections designed to reduce risks. For example, Purpose’s ETF stores assets in offline cold storage, which can only be accessed by authorized custodians — a significant deterrent against online hacking.

For Canadian investors, Bitcoin ETFs also offer a potentially diversified approach to entering the crypto market. Some ETFs incorporate a mix of digital assets, helping spread risk across multiple cryptocurrencies, which may reduce exposure to individual asset volatility.

Risks in Bitcoin ETF investing

While Bitcoin ETFs have grown in popularity, they remain susceptible to Bitcoin’s characteristic volatility. Industry experts, such as Colin White of Verecan Capital Management, argue that cryptocurrency remains a speculative asset, subject to extreme price shifts. Bitcoin ETFs, though diversified in some cases, do not eliminate the risks associated with high volatility in the crypto market.

Additionally, investors should consider ETF fees, which can reduce returns over time. Although ETFs that include a range of digital assets may help distribute risk, this structure does not fully shield investors from potential losses, especially in a turbulent crypto market.

Exploring Bitcoin ETFs in Canada: how to get started

Canadians interested in Bitcoin ETFs can consider these steps for a successful entry into the market:

Research available Bitcoin ETFs: Options such as Purpose Bitcoin ETF (TSX:BTCC), Evolve Bitcoin ETF (TSX:EBIT), and CI Galaxy Bitcoin ETF (TSX:BTCX) are listed on Canadian exchanges and offer various structures and security approaches.

Compare ETF fees: Bitcoin ETFs often come with management fees, so it’s wise to assess how these fees may impact long-term returns.

Evaluate security protocols: Check if the ETF’s assets are in cold storage, and understand how the provider handles asset custody and protection.

Align with financial goals: While Bitcoin ETFs make it easier to access crypto investments, they still carry risk. Aligning with one’s financial goals and risk tolerance is essential.

Consider tax benefits: Holding Bitcoin ETFs in accounts like RRSPs or TFSAs can offer tax advantages, potentially reducing capital gains tax on returns.

Bottom line: Bitcoin ETFs in a shifting financial landscape

Bitcoin ETFs offer Canadians a convenient and regulated way to participate in the cryptocurrency market, balancing accessibility with enhanced security measures like cold storage. As political developments drive renewed interest in Bitcoin, investors should be mindful of the risks posed by its volatility. For those who conduct thorough research and align their strategies with their financial objectives, Bitcoin ETFs could become a valuable part of their investment portfolio in today’s evolving economic environment.